You Don’t Need 3 Apps to Pay Your Friends: Why U.S. Payments Feel Broken

Written by Casey Ariel Dike’We’ve all been there.

Brunch wraps up. One person puts the meal on their card to make it easy on the server. Everyone nods appreciatively. Then comes the part that somehow still feels harder than it should.

“Apple Pay?”

“Oh, you don’t have an iPhone.”

“Cash App?”

“Ah… no.”

“Venmo?”

“Okay, Venmo.”

Awkward chuckles. Someone rolls their eyes. Someone else starts downloading yet another app.

This moment is so common that we barely question it. But we should.

Because paying your friends back for brunch should not require an app audit.

Things Don’t Have to Be This Way

In some parts of the world, it doesn’t.

Take Kenya.

Kenya’s mobile money system, M-Pesa, links digital wallets directly to phone numbers. If you have a SIM card, you have a wallet. The money in that wallet is liquid and widely accepted.

People pay for groceries with M-Pesa. They top up electricity meters with it. They buy water. They pay farmers on the side of the road for fresh produce. According to Forbes, nearly 59% of Kenya’s GDP flows through M-Pesa.

While the level of adoption is impressive, what’s even more notable is interoperability — the ability for money to move easily across people, merchants, and services without friction. When systems work together, liquidity is unlocked for everyone, almost effortlessly.

The U.S. Has the Apps, But Not the Flow

The United States isn’t lacking digital finance tools.

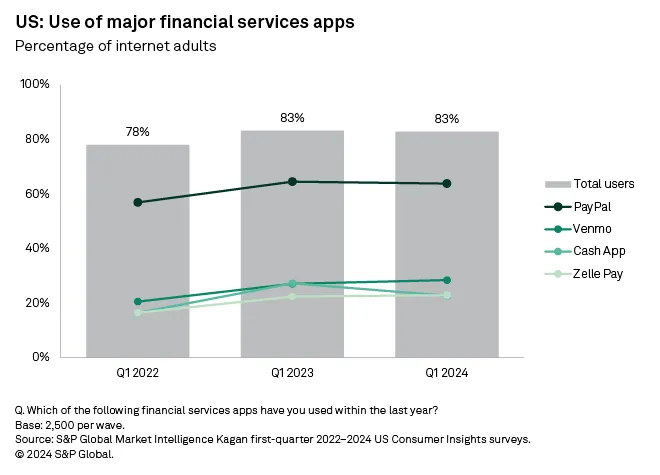

Eight in ten Americans use digital finance apps for online purchases, mobile banking, or digital payments. One in three Americans uses three or more financial apps. This level of penetration signals that trust and adoption are relatively high.

And yet, friction persists.

PayPal is used by roughly 64% of U.S. adults. But most PayPal users also use Venmo, Cash App, and Zelle. These platforms don’t talk to one another. Money can’t move freely between them. So users adapt.

They ask which app someone has. They switch between platforms. They create new accounts. They carry the burden of fragmentation themselves.

Even with this friction, 38% of Americans use digital wallets at least weekly, and 10% use them daily. One in five Americans regularly leaves home without a physical wallet, according to Capital One.The demand for digital wallets is here. What we’re grappling with is a systems problem — even if most consumers don’t have the language to name it.

What Happens When Interoperability Is Real

India offers a powerful case study.

In 2016, India launched the Unified Payments Interface (UPI), a system that allows banks and fintech apps to send money across platforms seamlessly. The results were so powerful, interoperability across UPI apps became mandatory one year later.

By August 2025, UPI processed more than 20 billion transactions per month, with values exceeding $300 billion. For a dominant fintech player, digital payment usage increased by over 50% in the year following integration. In geographically fragmented regions, both transaction frequency and transaction size rose sharply.

When friction disappeared, behavior changed.

People deserve infrastructure that gives them the freedom to move as they’d like to.

We already live this reality elsewhere.

Yahoo can email Gmail. Gmail can email Outlook. Outlook can email Hotmail. No one asks which provider you use before sending a message. The carrier doesn’t matter. And it shouldn’t.

Payments should work the same way.

This is the core idea behind open payments and interoperable systems: money should move as easily as information. Expecting this level of ease is not radical. It’s practical.

The Work Ahead

There are signs of progress.

In July 2025, PayPal announced PayPal World, a set of global partnerships aimed at connecting large payment systems and digital wallets. It’s a meaningful step forward. But this challenge is bigger than any single company.

True interoperability requires open systems, shared standards, and collaboration across sectors.

This has been the focus of the Interledger Foundation — advancing the idea that money should move as easily as an email.

Over the last five years, the Interledger Foundation has supported more than $21 million in grants, funding 271 projects across 42 countries that are building toward more inclusive, interoperable financial systems.

Perhaps seamless payments aren’t far-fetched at all.

Perhaps we’ve simply grown accustomed to the friction we shouldn’t accept.

In an age of digital commerce, we have the space to imagine better systems.

If you’re curious about how interoperable financial systems are being built, and how you might contribute, the Interledger Foundation invites you to explore the community and get involved.

Because no one should need three apps to pay their friends.

Casey Ariel Dike’ is the Founder and CEO of Blaze Group®, a finance innovation studio offering tools and frameworks that help overlooked communities own, protect, and scale their economic power. With a background in global corporate banking, Casey now focuses on reshaping capital access through financial education, fintech literacy, and equitable product design. She serves as a consultant for the Interledger Foundation, expanding their reach across financial institutions, colleges, and fintech communities concentrated in underbanked regions.